Expense Ratio in Mutual Funds: The Silent Fee That Shrinks Your Returns

Discover the everyday cost of mutual funds - and why it can quietly eat into your wealth.

Every middle-class investor’s confusion…

You invest Rs.1,00,000 in a mutual fund. You dream of a double-digit return in the long run. But when the statement arrives, something looks off.

The numbers are smaller. The dream feels shorter. And you ask yourself:

“Who is taking a bite from my returns? And why the money seems less than my calculations?”

That invisible bite has a name: Expense Ratio.

Our Characters

Hero: Bunny, a confused investor who represents everyone of us.

Guide: Investing Uncle, the calm voice who explains money with tea, humour, and truth.

The Problem - Bunny is confused

“Uncle, I invested in a fund that delivered 12% CAGR returns in 6 year. But my account shows money as per 11% CAGR! Where did the missing 1% go?”

Bunny looked like a man who bought an ice cream cone but got only the cone without the scoop.

The Guide Appears

I chuckle, SIP my tea, and said:

“Bunny, that missing slice of return is the Expense Ratio - the daily fee your fund charges to manage your money.”

The clear explanation

I explain slowly:

Expense Ratio = the annual cost of running a mutual fund.

It covers fund manager’s salary, research team, admin, marketing, operations.

Shown as a percentage of your investment (like 1% or 0.5%).

Not deducted once a year, but daily in small bites from the NAV.

You don’t pay separately; it’s already built into your fund’s price.

Example:

Rs.1,00,000 in a fund with 1% expense ratio = about Rs.1,000 a year (=Rs. 2.7 per day). Small today. Big tomorrow.

Making the explanation Tea Friendly (The Tea Analogy)

I took Bunny to a tea stall.

“Look, Bunny. Here the Tea costs Rs.10, and ‘It includes Re.1 for the cup and service’.

That Re. 1 is the Expense Ratio.

You don’t pay it separately. It’s already built into the Rs.10.

Now, imagine you drink tea every day for 20 years. That extra Re.1 adds up to a big number.

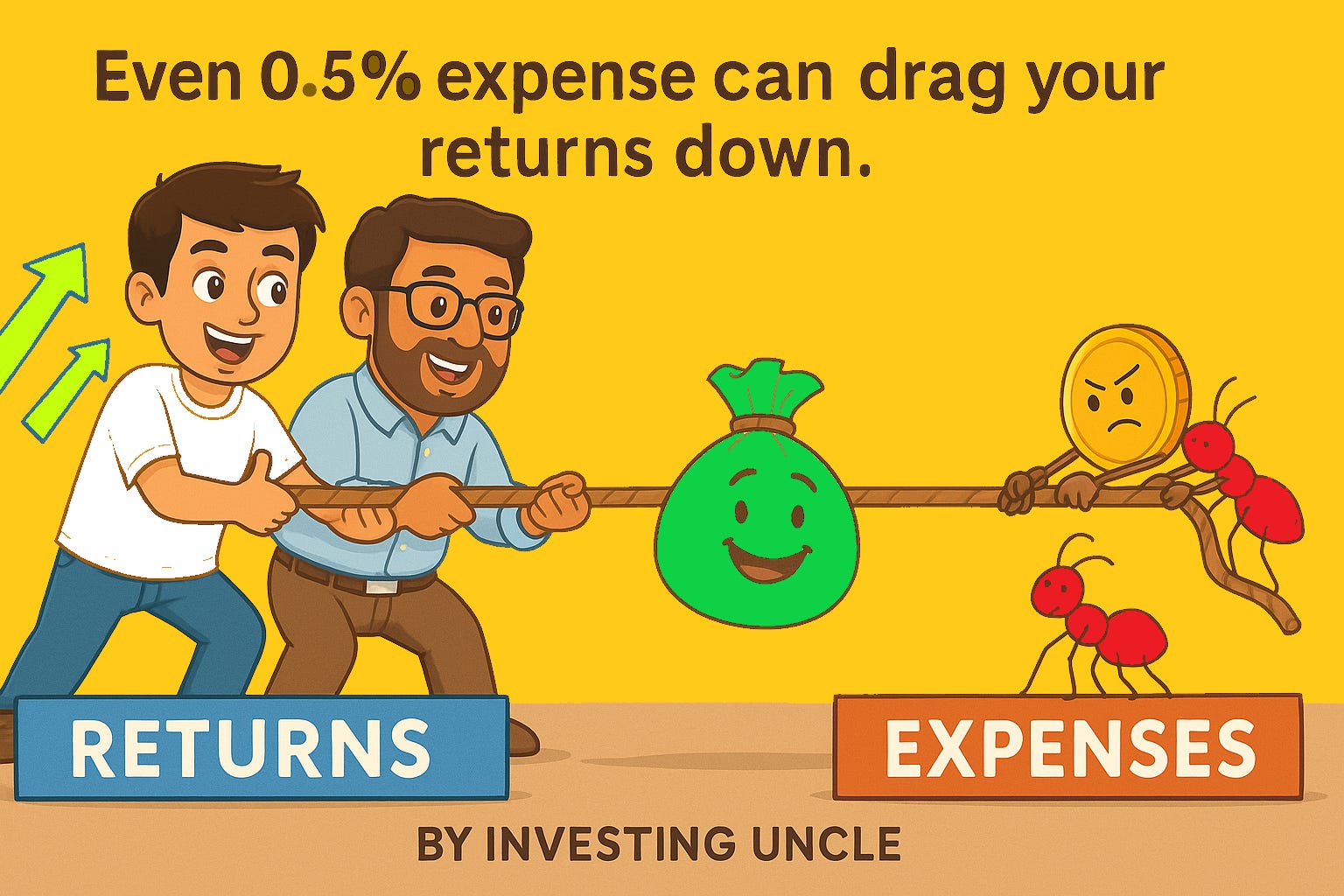

Expense Ratio works the same way. A 0.5% difference looks tiny today but can eat lakhs over decades.

Active funds = café tea (costlier, because of extra staff and fancy service).

Index funds = roadside tea (simpler, cheaper, still does the job).

The lesson? Always check the ‘tea service charge.’ The less you pay, the more tea (returns) you enjoy.”

Transformation - Bunny understands

Bunny’s jaw drops.

“Uncle! So my fund’s performance is one side, but the expense ratio is like a slow leak. It quietly drains my wealth!”

I pat his back.

“Right, Bunny. Wealth isn’t eaten by a tiger in one bite - it’s takes small bites away quietly, like ants stealing sugar from your Tea cup.”

Reader (Bunny) Feels Empowered

Bunny smiles with confidence.

“From today, I’ll always compare expense ratios. If two funds look similar, I’ll choose the one that costs less.”

And that, dear reader, is your transformation too. If Bunny can learn, so can you.

Why You Should Care About Expense Ratio

A 0.5–1% difference compounds into lakhs over decades.

Expense ratio is deducted daily, not once a year.

Active funds = higher expense ratios.

Index funds/ETFs = much lower expense ratios.

Always balance cost vs. performance when choosing funds.

For more on this, revisit Uncle’s earlier blog…

Book Summary: The Little Book of Common Sense Investing (John Bogle’s Wisdom Explained).

…John C. Bogle’s entire life mission was to save investors from high costs.

Reader = Real Hero

Bunny no longer looks scared. He walks away smiling, armed with new wisdom.

And you, too, are no longer in the dark.

You now know that Expense Ratio is just a service fee. And the smarter you are with it, the richer your future becomes.

“In investing, it’s not the big feast that makes you fat - it’s the small biscuits you munch daily without noticing.”

Share your thoughts in the comments, subscribe for more Sunday wisdom, and let’s meet again.

See you next Sunday at 09:15 AM.

Did this blog bring clarity? I hope it made you smile and feel a little wiser about your money.

If yes, maybe you can treat Uncle with a cup of tea?

Disclaimer: Mutual fund investments are subject to market risks, read all scheme related documents carefully before investing. The past performance of the mutual funds is not necessarily indicative of future performance of the schemes. Investors are requested to review the prospectus carefully and obtain expert professional advice with regard to specific legal, tax and financial implications of the investment/participation. This blog/Website is for Educational purpose only. Any reference should not be treated as any form of Financial Advice.

Any person referred to in this post is purely coincidental. The characters, names, and situations mentioned are for illustrative and educational purposes only and are not intended to represent any real individual.

‘Investing Uncle’ is NISM Series V-A Certified (Mutual Fund Distributor’s Certification Examination) conducted by National Institute of Securities Markets (NISM).

Investing Uncle is not SEBI/AMFI Registered.